For those operating under a Besloten Vennootschap (BV), the era of treating paperwork as a "later" task has ended, replaced by a regulatory environment that demands technical precision and digital transparency.

The BV is Not a Magic Cloak

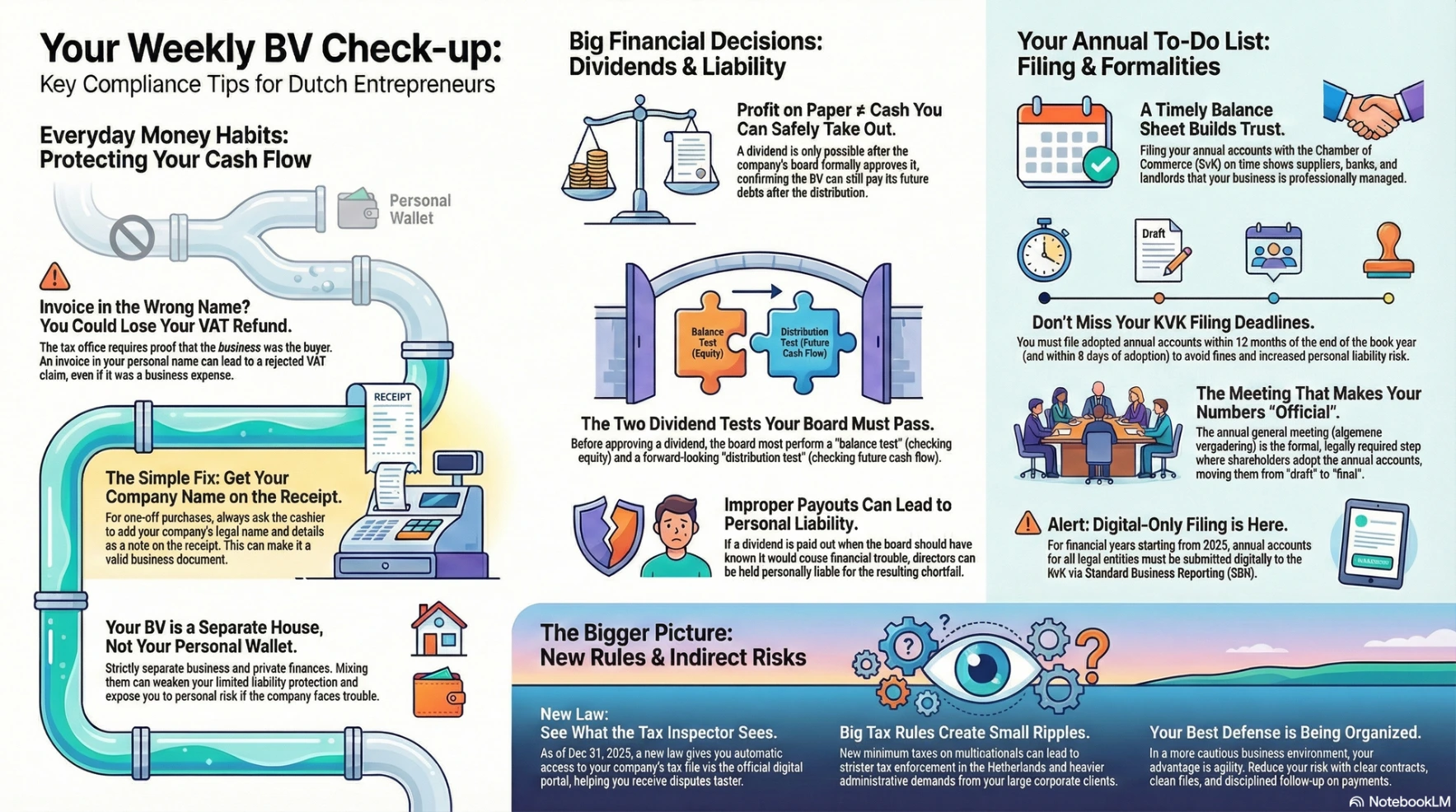

Many small business owners establish a BV for the protection of limited liability, yet this protection is a "deal" that requires the director to act responsibly.

Under the administratieplicht (legal duty to keep records), a BV only shields your private life if you treat it as a separate entity with its own clear boundaries.

If the administration is opaque, or if business and private funds are mixed, the law may look past the company structure to the person behind it, potentially leading to bestuurdersaansprakelijkheid (director’s liability).

The VAT Trap:

Names and NotesA recurring compliance leak for micro-businesses involves the simple act of naming.

To successfully reclaim VAT, the Dutch Tax Office requires proof that the business is the buyer; if a contract or invoice is in your personal name, the claim is often rejected during an audit.

Even for small, one-off purchases, "VAT is on the receipt" is not the finish line.

For these instances, compliance experts recommend adding company details as a note on the receipt at the point of sale or requesting a proper invoice immediately to avoid "silent leaks" in cash flow.

The 2025 Filing Revolution:

SBR and Digital AccessFor the 2025 book year (filed in 2026), the Chamber of Commerce (KvK) has mandated that annual accounts must be submitted via SBR (Standard Business Reporting).

This means that simply uploading a PDF is no longer an option; your software and workflow must support this technical standard.

Furthermore, the Wet stroomlijning fiscaal inzagerecht, effective as of 31 December 2025, is flipping the logic of tax transparency. Instead of having to "chase" the Inspector for information, businesses are moving toward automatic digital access to their own tax files through the Tax Administration’s portal.

However, this "right to inspect" only provides value if your internal dossier, contracts, bank movements, and agreements, is ready to be matched against the government’s data.

Dividends:

The "Reality Check"As owners look to distribute 2025 profits, it is vital to remember that a dividend is not a guaranteed payday. In the Netherlands, a distribution requires both a balanstest (balance test) to protect statutory reserves and a uitkeringstoets (distribution test) to ensure the BV can meet its future obligations.

If a board approves a dividend while knowing the company cannot pay its upcoming bills, the directors can be held personally liable for the resulting shortfall.

Global Ripples, Local Admin

Even international shifts, such as the 15% minimum tax for multinationals, are creating "ripples" for the Dutch small business. Large corporate clients, reacting to a more cautious tax environment, are tightening their internal controls. Small suppliers should expect stricter onboarding processes, thicker contracts, and increased requests for compliance documentation.

Summary for the Week

Success in this environment is not about complexity, but about steadiness. Closing the year cleanly, reconciling banks, confirming VAT positions, and formalising shareholder loans, reduces the noise that leads to expensive surprises.

A BV is like a house: it provides shelter from the elements, but only if you keep the doors locked, the windows maintained, and the boundary lines clearly marked. If you treat the walls as if they don’t exist, the wind will eventually find its way inside.